The Global Exchange Rate Map under the Background...

Title: The Global Exchange Rate Map under the Background of the Great Divergence of Interest Rates

In the context of the start of another global financial cycle and the divergence of policies of major economies,the trend of the renminbi exchange rate in 2022 has attracted much attention. The renminbi has performed very well in the past two years,with an appreciation of 6.1% against the US dollar in 2020 and another 2.8% in 2021,for a total of nearly 9%. Considering that the United States has accelerated the pace of monetary tightening in order to curb inflation and China is opening the gate to easing to prevent economic downturn,the intuitive reaction is: after two consecutive years of sharp rises,should the renminbi depreciate a little this year? The very acceptable results also reflect the characteristics of two-way fluctuations. But sometimes intuition requires careful scrutiny,because forecasting exchange rates has always been an extremely risky business. The literature shows that in the 50 years since the collapse of the Bretton Woods System in the early 1970s,even the esoteric economic models built for exchange rate forecasts have not performed well. This article begins with a brief introduction to the historically famous Meese-Rogoff puzzle that proved unpredictable exchange rates,and compares two instances where the predicted exchange rate deviates significantly to illustrate why it is so difficult to predict exchange rates. After that,based on the detailed description of the global exchange rate map under the current great divergence of interest rates,an analytical framework for studying the future trend of renminbi and the US dollar under the dynamic game of multiple factors is given.

What is the Meese-Rogoff puzzle?

This is a true story. Kenneth Rogoff,now a professor of economics at Harvard University,found a job at the Federal Reserve after graduating with a Ph.D. from MIT in 1980. The boss asked him to do exchange rate forecasts. So he co-authored an article with Richard Meese and came to the depressing conclusion: in the short term,from a few months to a year,the exchange rate is unpredictable,and the performance of many models is not as good as a random walk. The paper,published in 1983,is still widely cited and has become a classic. And its conclusion is known as the Meese-Rogoff puzzle,that is,even though you know that the exchange rate cannot be predicted,but you still pay an economist to predict it.Why spend money in vain! After the Meese-Rogoff paper,a slew of studies continued to explore this question,but it was always difficult to build confidence in exchange rate forecasts - although the accuracy improved slightly over time spans of more than a year.

Two examples of deviations in exchange rate forecasts

In 2017,the Federal Reserve raised interest rates three times. The US economy was strong. Corporate profits were huge and the stock market rose sharply. However,the US dollar index plummeted by more than 10%,which surprised many bullish forecasters. At the end of October of that year after the dollar had fallen deeply,Jason Furman,a professor at Harvard University and former chairman of the Council of Economic Advisers during the Obama Administration,argued in a speech on tax reform that,driven by the Federal Reserve's monetary tightening and Trump's tax cuts,the dollar would appreciate. Unexpectedly,the dollar has since accelerated its decline for several months. In early March 2018,another Harvard professor,Larry Summers,wrote an article reflecting on why the dollar did not rise but fell. He argued that the combination of factors such as better economic performance in Europe and other countries,Trump's advocacy of a weak dollar,the US has achieved full employment but an increase in the fiscal deficit,and the trade war have made investors lose confidence in the dollar. Although interest rates in the United States are much higher than those in Europe,it is still difficult to reverse the decline.

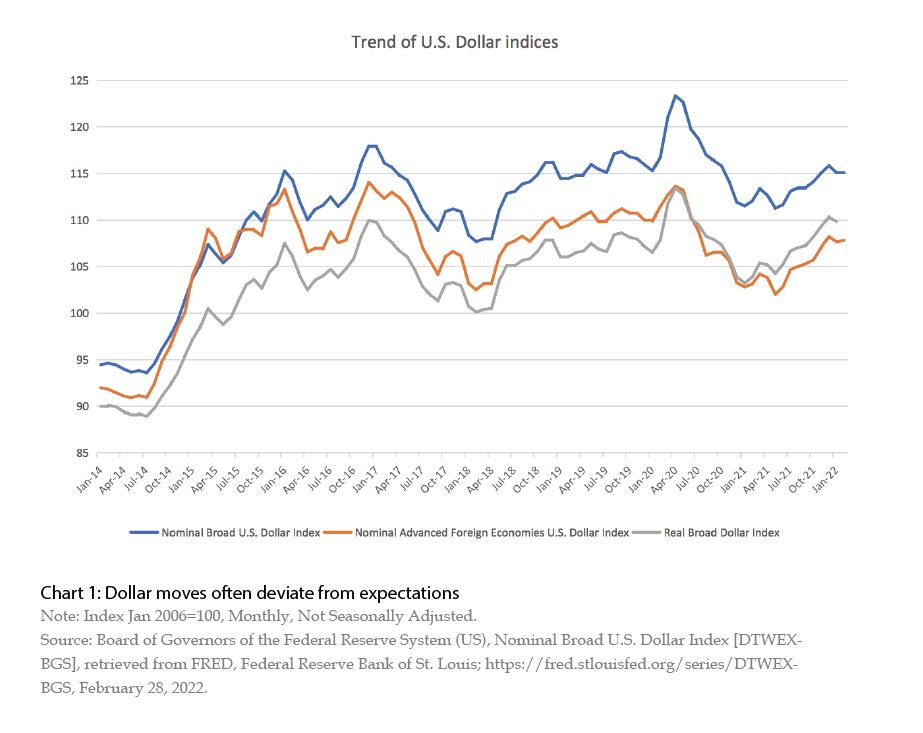

Coincidentally,Stephen Roach,a faculty member at Yale University and former chairman of Asia and chief economist at Morgan Stanley,wrote an article in June 2020,predicting that the US dollar will depreciate by 35% by the end of 2021. In the rest of the year,the U.S. dollar index did depreciate by more than 10%. In January 2021,Roach was full of confidence and reiterated his prediction in an article titled "The Dollar's Crash Is Only Just Beginning",

but the U.S. Dollar Index for the full year of 2021 rose by 6.7%. (See Chart 1)

Therefore,forecasting the exchange rate is really a difficult task,and the participants need to be not only brave but also humble,even if they have thought about it,they should not forget to look before they leap.

It's worth adding that while the US dollar fell sharply for five months from October of 2017 to March of 2018 after professor Furman's prediction that the US dollar would strengthen,it has turned sharply higher since April 2018 all the way to the end of that year. So Furman was not entirely wrong,it just further illustrates the difficulty of predicting exchange rates in the short term.

The global exchange rate map under the great divergence of interest rates

At present,as the monetary policies of major developed economies represented by the U.S. begin to turn, a new round of global financial cycle has begun. Against this backdrop,some countries have started to tighten their monetary policies to curb asset price bubbles and inflation while also preventing capital outflows and exchange rate fluctuations. However,a considerable number of central banks remained unmoved and continued to maintain policy stability,and a few even turned on the door of monetary easing. The superposition of the above has created the current situation of sharp differentiation of interest rates.

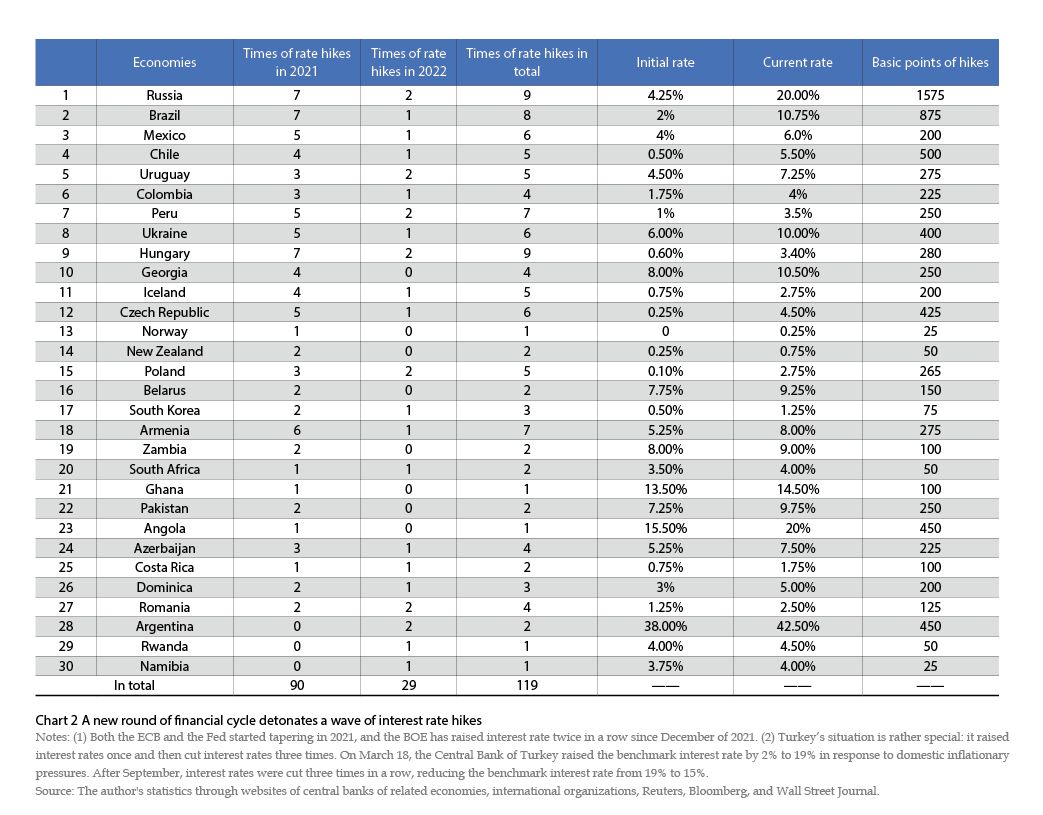

According to the author's incomplete statistics,excluding the UK,from the beginning of 2021 to February 28 this year,a total of 30 economies have raised interest rates 119 times. (See Chart 2) Among them,27 economies have raised interest rates 90 times in total in 2021,and 22 economies have raised interest rates 29 times in total so far this year. Russia and Hungary topped the list with 9 rate hikes,Brazil hiked rates 8 times,Peru and Armenia each raised rates 7 times,Mexico and the Czech Republic raised rates 6 times each,while Chile,Uruguay,Ukraine,Iceland and Poland 5 hikes.

Horizontally,few economies in Asia raised interest rates,presumably mainly because inflation is more benign than elsewhere. But South Korea is a notable exception: not only did it raise interest rates on August 26 last year,becoming the first advanced economy to raise interest rates since the outbreak of the COVID-19 pandemic,but it has raised interest rates another two times in a row since then. The Bank of Korea raised interest rates in August last year mainly because it wasworried about asset bubbles. And now inflation has become a more important consideration.

In addition,some economies have tightened their monetary policies by means other than raising interest rates. Australia discontinued its yield curve control policy in 2021 and ended its A$350 billion bond purchase program in February of 2022. Singapore,in October of 2021 and January of 2022,unexpectedly raised the rate of appreciation of its main currency band twice in a row,and the second one was its first unscheduled action since 2015.

Of course,there are also many countries in no hurry to tighten monetary policy. Most prominent,of course,is China,which opened the door to easy money earlier last year. The Bank of Japan said that considering the economy had just recovered from the COVID-19 pandemic,it would not tighten prematurely. Many Asian economies have not yet tightened,but as inflation rises and the cycle turns,whether they will follow suit in the future is worth watching closely. In Europe,unless the situation is urgent,the European Central Bank is reluctant to raise interest rates anytime soon this year. And the Riksbank has made it clear that it will implement a zero interest rate policy until 2024.

Then,in the above-mentioned situation of the great divergence of interest rates,are the exchange rate movements of various economies also very different? With this idea in mind,the author systematically sorted out the ups and downs of the foreign exchange market so far this year,and obtained the following interesting findings.

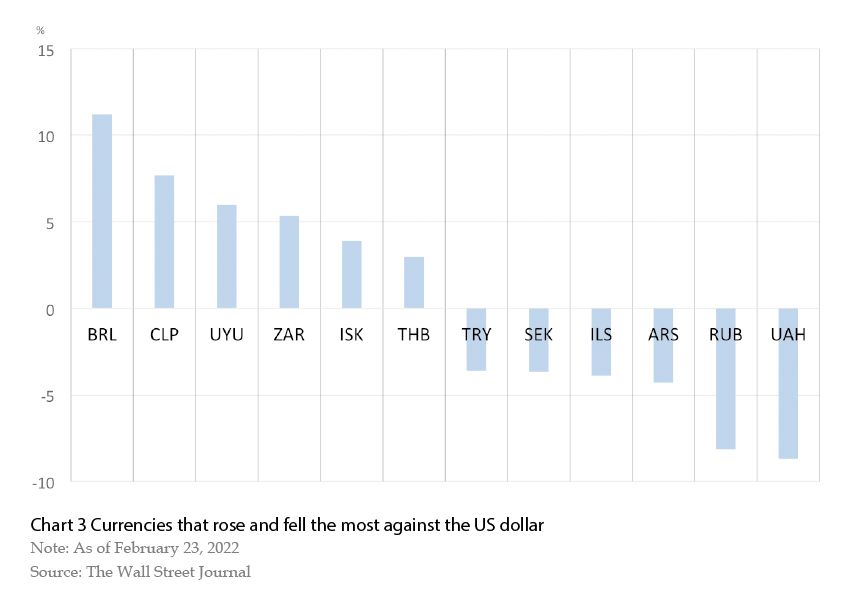

Let's start by looking at what the biggest currency winners are. As of February 22 this year,there were six currencies that rose more than 3% against the US dollar: the Brazilian real rose 10.1% against the USD,ranking first,the second-ranked Chilean peso rose 7.5% against the USD,and the South African rand,the Uruguayan peso,the Icelandic krona and Hungarian Forint came in third to sixth place,gaining 5.8%,4.3%,4.1% and 3.4% against the US dollar,respectively. Interestingly,these six countries have all raised interest rates on a precautionary basis since last year. Except for South Africa,which raised interest rates twice,the other countries have raised interest rates no less than five times.

Interestingly,there are also six currencies that have fallen by more than 3% against the US dollar,ranked by the size of the decline: the Ukrainian hryvnia,the Russian ruble,the Argentine peso,the Israeli shekel,the Turkish lira and the Swedish krona,with a range of -6.2%,-5.1%,-4.2%,-3.7%,-3.4% and -3.0%,respectively. (See Chart 3)

In-depth analysis shows that although Russia and Ukraine have raised interest rates 8 and 5 times respectively,the Ukrainian hryvnia and Russian ruble depreciations are widely expected because they are at the core of the current geopolitical conflict. For Argentina,its inflation rate is as high as 50%,though since last year,the benchmark interest rate has been raised twice to 42.5%,but the real interest rate is still negative. Another thing is that it is still difficult to determine if the IMF's massive financial assistance to Argentina would work well,and if so,when. The fall in the Argentine peso is a comprehensive reflection of these factors. Turkey's response to high inflation by cutting interest rates is counterintuitive,and it would be surprising if the currency didn't depreciate. Israel's economy grew by 8.1% last year,but the CPI rose 3.1% in January this year,exceeding the upper limit of its inflation target of 1% to 3%,but its benchmark interest rate remained at a low of 0.1%,so the currency is difficult to strengthen. The Riksbank ended its asset purchase program at its meeting on November 25 of 2021,but announced that it will not raise interest rates until 2024 to maintain its current zero interest rate policy. The ECB's reluctance to raise rates prematurely was similar to that of the Riksbank,which drove euro fall 0.4% against the US dollar.

Of course,the analysis of exchange rate fluctuations also needs to broaden the horizon,and should not be limited to the current period. For example,South Korea is the first developed economy to raise interest rates since the outbreak of the COVID-19 pandemic,and has raised interest rates three times since August 26,2021. If you only look at this year,the Korean won has fallen against the US dollar by 0.3%,but if it is calculated from the beginning of June last year,the won rose 7.6%.

The author has repeatedly emphasized that interest rates are not the single determinant of exchange rates. However,comparing various currencies against the background of the divergence of global interest rates,combined with a comprehensive analysis of many other factors such as inflation,economic performance,pace and expectations of monetary tightening,fiscal policy orientation and even geopolitics,can provide a very intuitive yet informative viewing window for studying exchange rates.

Ups and downs of renminbi and the US dollar under the dynamic game of multiple factors

Regarding the factors affecting the trend of the U.S. dollar,in addition to the tightening of monetary policy by the Federal Reserve,there are three other key points of concern: first,whether inflation can be controlled sooner; second,whether the COVID-19 epidemic situation can be improved quickly in the country; third,whether the nearly US$2 trillion fiscal bill pushed hard by the Biden administration can be passed. If the answer to all three of the above is yes,there is a high probability that the US dollar will appreciate.

In terms of renminbi,although monetary easing has compressed the interest rate gap between China and the U.S.,there are five supporting factors still: first,inflation in China is much lower; second,active fiscal policy is underway; third,China has been vigorously promoting financial opening and renminbi internationalization; fourth,potential financial risks are being resolved,manifested in the stabilization of the real estate sector and the room for lifting a bit in macro leverage ratios; fifth,despite being fragmented by the COVID-19 pandemic,China still has supply chain and export advantages.

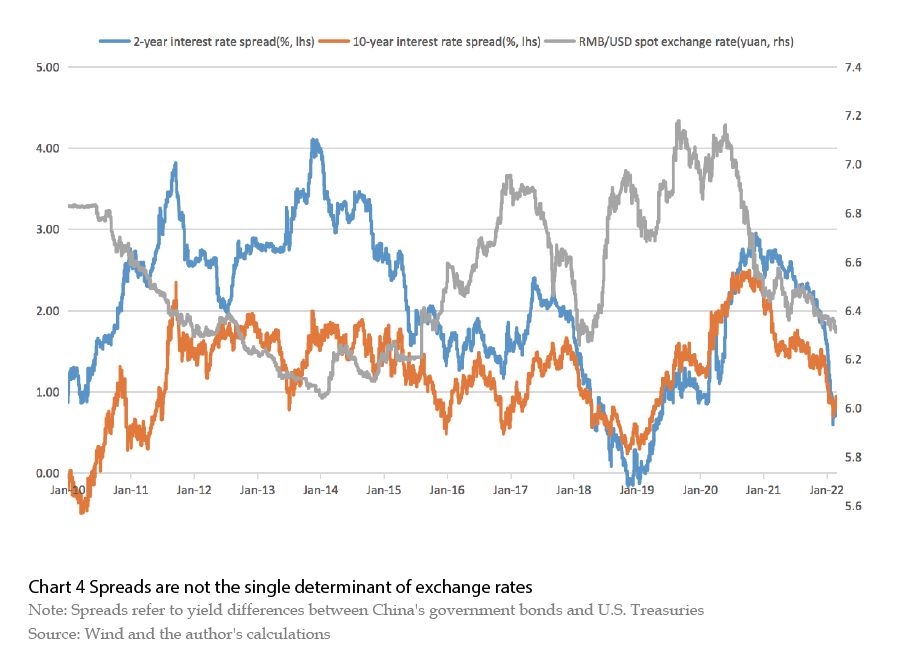

A question that has been frequently asked recently: Why is the interest rate gap between China and the U.S. narrowing while the renminbi continues to appreciate against the US dollar? (See Chart 4)

The author's answer is: first,the interest rate differential is not the single determining force of the exchange rate; second,on the U.S. side,factors such as the inflation is rising while the Fed's attitude to curb inflation is still not firm,the COVID-19 epidemic is far from being controlled,and the obstruction of Biden's nearly US$2 trillion fiscal bill have all played a role; third,on the renminbi side,there are five factors mentioned above that support it. Looking at the whole year,all of the above elements affecting the renminbi and US dollar will be in a dynamic game. Coupled with the impact of potential geopolitical conflicts,the exchange rate in 2022 is destined to be full of suspense.

The author is a Ph.D in economics,senior guest research fellow at National Institute for Finance and Development (NIFD),former managing director at CITIC Securities